On Nov. 7, 2006, Michigan voters will be asked to consider a proposed new law that would, if passed, require annual state spending to increase at no less than the inflation rate for the following state budget areas: public school districts and charter schools; certain specific budget items in state spending on public school districts and charter schools; and state universities and community colleges. The proposal also contains new requirements for state payments to districts with declining enrollment and places liability for school employee pension cost increases on state government, rather than school districts. The proposed new law will appear as “Proposal 5”on the ballot, and its mandates would take effect in the 2006-2007 school year.

On Nov. 7, 2006, Michigan voters will be asked to consider a proposed new law that would, if passed, require annual state spending to increase at no less than the inflation rate for the following state budget areas: public school districts and charter schools; certain specific budget items in state spending on public school districts and charter schools; and state universities and community colleges. The proposal also contains new requirements for state payments to districts with declining enrollment and places liability for school employee pension cost increases on state government, rather than school districts. The proposed new law will appear as "Proposal 5"on the ballot, and its mandates would take effect in the 2006-2007 school year.

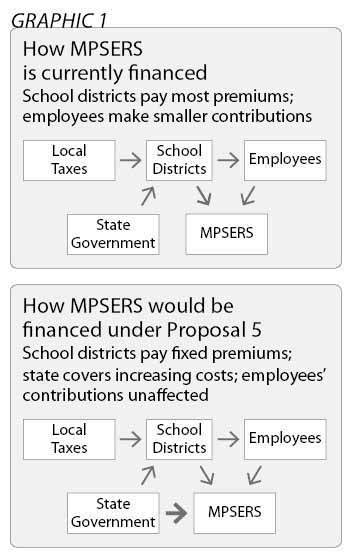

During the recessionary period from 2001 to 2005, Michigan state government’s spending on primary and secondary education did not keep pace with inflation.* Nevertheless, it did increase slightly during this period. Moreover, state school aid fund spending in 2005 was more than 40 percent higher than in 1995 — about $1 billion above the 27 percent total inflationary growth for that period. State school aid spending easily remained the single largest expenditure of state government.

Michigan is still one of the nation’s leaders in school spending. According to the federal government’s National Center for Education Statistics, Michigan’s per-pupil spending in 2003 was ninth in the nation, and according to the National Education Association, the average salary for Michigan instructional staff was eighth. In 2004, the average compensation for instructional staff at Michigan public schools was more than $54,000. If one of Proposal 5’s main goals is to ensure high and rising primary and secondary school spending over the long term, it would seem that goal has already been met.

|

* Sources for the findings cited in the “Executive Summary” are provided in endnotes to the main text of the Policy Brief. |

State appropriations for community colleges and universities were nearly 37 percent higher in 2001 than in 1995, compared to 15 percent total inflationary growth. State higher education expenditures dropped nearly 10 percent between 2001 and 2005. Yet Michigan’s public universities and community colleges were able to raise money from tuition and other sources; total expenditures from the general funds of the four-year universities increased every year from 2001 through 2005. Spending per capita by Michigan’s public institutions of higher education was ninth in the nation in 2002 — nearly 33 percent above the national average.

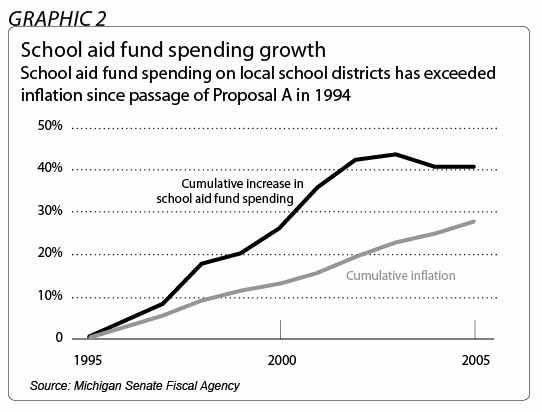

It is also worth noting that even as the growth in state appropriations for universities exceeded the inflation rate between 1995 and 2001, the average undergraduate in-state tuition at Michigan universities rose more than 28 percent — an increase of nearly twice the inflation rate. Thus, while Proposal 5 might ameliorate tuition hikes, it is unlikely to solve the problem of rapidly rising tuition.

The pension and retirement health care provision of Proposal 5 involves a state-administered retirement plan primarily for employees of Michigan public school districts. A recent, credible estimate suggests that the cost of the retirement plan will increase more than 94 percent by 2016. In contrast, the cost increase from 1996 to 2006 was about 50 percent. The total retirement fund contribution increases from 2004 through 2006 cost the average school district an additional $178 per pupil, exceeding the state’s per-pupil foundation allowance increase during the period by $3 per pupil.

The major factors driving the hike in retirement costs are a growing imbalance in the number of workers supporting retirees, the need to recover recent stock market losses, and a substantial projected payment increase for the retirement health care benefit. While the cost of the health insurance benefit represented less than 45 percent of retirement fund contributions in 2005, it is projected to reach more than 62 percent in 2020.

The proposal does not change the retirement fund cost structure, even though the substantial majority of private-sector employers do not offer any retirement health care benefit at all. Instead, Proposal 5 would shift nearly all of the future retirement fund cost increases from the budgets of school districts to the state. If Proposal 5 were to pass, the state general fund budget would assume responsibility for $386.3 million of an estimated $1.9 billion total retirement fund cost in fiscal 2007 alone. This $386.3 million figure is in fact larger than 16 of the 26 state departmental budgets from fiscal 2006.

By putting the financial pressure of rising retirement contributions on state government, Proposal 5 would make local budgeting easier, but would also subsidize school districts’ personnel budgets by reducing the local cost of payroll. This subsidy could lead districts to make otherwise unsustainable staffing decisions and drive overall retirement liabilities even higher.

State lawmakers had the discretion to cut some programs more than others during the current recession. Proposal 5 would leave lawmakers with less flexibility during future declines in state revenue growth. State spending on education at all levels represents 54 percent of the state budget that depends on state revenues. Proposal 5 would mandate that this spending rise with inflation regardless of the funds available for the remaining 46 percent.

Proposal 5 would provide lawmakers an incentive to cut state spending on certain primary and secondary education programs, such as adult and vocational education, by an estimated $141.7 million in fiscal 2007. Indeed, the Michigan Senate Fiscal Agency has assumed such cuts would take place, and these cuts lower the first-year cost estimate for Proposal 5 to $566.6 million. Without the cuts, the estimated first-year cost would reach $708.3 million. Assuming no increase in taxes, legislators could meet Proposal 5’s 2007 spending requirements in one of two ways: by making 9.8 percent cuts to noneducation general fund spending, such as human services, corrections or veterans services; or by making 7.9 percent cuts to this spending and $141.7 million in cuts to the "unprotected" primary and secondary education spending noted above.

Tax increases could also be used to raise some or all of the first-year spending required by Proposal 5. In the case of the income tax, $708.3 million would represent about 11.1 percent of current revenue, while $566.6 million would represent 8.9 percent. Raising taxes on Michigan households, however, would decrease their disposable income and raise the effective cost of such things as higher education.

Colorado’s experience with a similar state education spending mandate suggests that tax increases, spending cuts to noneducation programs, or both are reasonably likely to occur if Proposal 5 is passed.

There is no apparent correlation between Michigan’s high spending for education on the one hand and brighter kids and more jobs on the other. Despite the relatively high level of Michigan’s spending on education, Michigan students have posted mediocre standardized test scores, and Michigan’s economy is now one of the nation’s worst. Economist Richard Vedder recently found no association between state spending on higher education and economic growth.

Proposal 5 could produce unintended educational effects. Granting additional money to districts with declining enrollment could insulate poorly performing districts from the financial consequences of their failures. This reduced penalty, along with the proposal’s spending increases regardless of academic performance, could lower poorly performing districts’ incentives to reform.

On Nov. 7, 2006, Michigan voters will be asked to consider a proposed new law that would, if passed, predetermine certain financial priorities for state government by mandating annual increases in state spending for education at all levels. The proposal also contains requirements for new state payments to districts with declining enrollment and places increased liability for school employee pension costs on state government, rather than school districts. The proposed new law will appear as "Proposal 5" on the ballot.

Proposal 5 is not a proposed amendment to the state constitution; it is a citizen "initiative," as described in Article 2, Section 9 of the Michigan Constitution. This constitutional provision allows citizens to draw up proposed laws, gather registered voters’ signatures in support of the proposal and submit them to the Legislature for approval or rejection "without change or amendment" within 40 session days. If the Legislature fails to approve the citizen initiative, the proposal is presented to the state’s voters at the next general election.

Proposal 5 was submitted to the Legislature by the "K-16 Coalition for Michigan’s Future," an alliance of public education employee unions and representatives of parent organizations and public education institutions, including the Michigan Education Association, the Michigan Parent Teacher Student Association and the Michigan Association of School Boards. In this instance, the Legislature did not approve (or reject) the proposal. If Michigan voters pass the proposal on Nov. 7, it will become law, and the Legislature will not be able to repeal or amend it unless three-fourths of both the Michigan House and the Michigan Senate support the change.

The proposal’s mandates would take effect in the 2006-2007 school year. Because the Legislature has already approved the fiscal 2007 budget, which covers this school year, lawmakers would be required to revise the budget and make additional payments to educational institutions if voters approve the proposal.

The brief ballot summary and exact text of Proposal 5 appear in an appendix at the end of this study. In plain language, Proposal 5 would create the following spending requirements:

Mandated Spending Increases for "K-16" Education Budgets

The proposal would require annual state spending to increase at no less than the rate of inflation in two major areas of education spending by state government:

total spending for public school districts and charter schools(primary and secondary education), and

total spending on universities and community colleges.

Note that these provisions do not limit the money raised by local property taxes to service school district debt for construction and capital expenses. Local property taxes would continue to increase or decrease in accordance with the outcome of local bond elections and constitutional limits on property tax rates.

Proposal 5 would also mandate that state spending on education would increase at no less than the rate of inflation for four main components of state spending on public school districts (item No. 1 on the list above):

the per-pupil foundation allowance paid to districts and charter schools for each student;

"at-risk" pupil spending;

special education spending; and

intermediate school district operations spending.

These four provisions mean that state government would provide at least an inflationary increase not just in primary and secondary state education spending as a whole, but also in each of the listed subcategories. Primary and secondary education spending that did not belong to the list of four budget areas could decrease or grow at less than the inflation rate, as long as total primary and secondary spending still matched or exceeded inflation.

As noted above (in item No. 2 in the first list), total annual state spending for Michigan’s public universities and community colleges would also receive an annual inflationary spending increase. This mandate, however, would not apply to each individual school. Thus, annual spending for some universities could increase by more than inflation, while spending for others could increase by less (or decrease), as long as the total spending in the higher education budget increased by at least the inflation rate. The same would be true for schools that received their state funding from the community colleges budget.

New Spending Requirements

Proposal 5 would create two new spending requirements for the state’s education budget:

additional state foundation payments to districts with declining enrollment, and

a decrease in disparities in state funding between school districts.

The first of these involves an adjustment to the current method of funding school districts. Under present law, most of the money distributed from state government to local school districts is provided through a per-pupil "foundation allowance." School districts are required to report accurate counts of their student population each year, and state government then pays most districts based on the pupil counts.

About 11 percent of the state’s districts, however, currently receive their per-pupil foundation allowance based not on the usual counts, but on the average of the districts’ counts in the current year and in the previous two years. These districts qualify for this alternative payment method through their low population densities, small enrollment (fewer than 1500 students) and ineligibility for special state monies for geographically isolated areas, such as islands.[1]

Proposal 5 would extend the alternative payment option to any district wishing to use it. Since the three-year formula would include student counts from previous years, it would increase the state money that districts with declining enrollment received. Districts with stable or increasing enrollment, on the other hand, would remain free to receive their per-pupil foundation allowance based on their current student enrollment.

Proposal 5’s second new spending provision would speed up the process of reducing the funding differences between Michigan’s higher-spending public school districts and lower-spending school districts (and charter schools). Some reduction has occurred since the passage of Proposal A in 1994, but Proposal 5 would further the decrease so that the difference between the foundation allowances for the higher-spending and lower-spending districts would fall from the current $1,300 per pupil to $1,000 per pupil by fiscal 2012.[2]

A Transfer of Responsibility for School Employee Pension Cost Increases

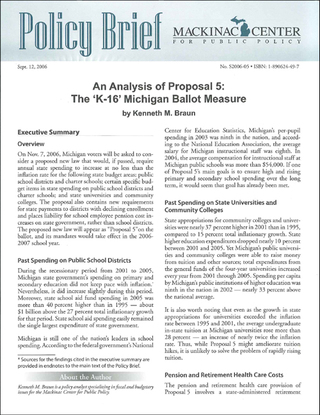

Proposal 5 would also shift payment responsibilities for the Michigan Public School Employees Retirement System. MPSERS is the state-administered retirement plan for employees of Michigan’s local and intermediate school districts and for employees of some public universities, community colleges, charter schools and libraries. Public school districts, intermediate school districts and these districts’ employees make up more than 90 percent of payments into MPSERS.[3]

MPSERS is for the most part a conventional "defined-benefit" retirement plan. MPSERS is managed by the Michigan Office of Retirement Services and is governed by an appointed board representing various school and government stakeholders. The MPSERS staff, with guidance from the board, selects where and how to invest pension funds, and education retirees receive a fixed payment after retirement based upon their years of employment and salary history.[4] Additionally, MPSERS enrollees are eligible to receive a retirement health care benefit for themselves and their dependents at a discount, paying less than 15 percent of the actual premium cost of their medical insurance from the time of retirement until they are old enough to receive federal Medicare benefits.[5]

MPSERS funding comes from two sources: public school districts and their employees. Employees contribute a refundable percentage of their pretax salary to the pension fund. Public school districts — the employers — provide the substantial majority of the funding. The school district’s payment is calculated as a percentage of payroll and is set by the MPSERS board at a level that is actuarially determined as necessary to keep the MPSERS fund solvent.

For the 2004-2005 school year, the rate was set at 14.87 percent of total payroll, with 8.32 percentage points distributed to the pension fund and 6.55 percentage points distributed to the health care fund. Local school districts now pay the MPSERS obligation directly, primarily with money sent to them by the state.

Local school districts assumed their current MPSERS responsibilities in 1995, following the passage of Proposal A, the landmark state education finance reform proposal of 1994. Since then, the districts’ annual MPSERS contribution rate has fluctuated from a high of 14.92 percent of pretax payroll (during 1997) to a low of 10.68 percent of pretax payroll (the following year).[6]

Proposal 5 would change this system for fiscal 2007 and beyond. Under the proposal, local school districts would pay the lesser of two amounts: four-fifths of the total employer MPSERS contribution, or 14.87 percent of pretax payroll. Any additional monies needed to maintain MPSERS’ financial viability would be paid from the state of Michigan’s general fund budget. For instance, under the current MPSERS payment formula, school districts’ expected contribution rate is 17.74 percent of payroll in fiscal 2007. Under the proposal, school districts would pay about 14.19 percent of payroll (four-fifths of 17.74), with the difference, approximately 3.55 percent of payroll, paid directly by state government. School employees’ payments to MPSERS would not change under the proposal.

Proposal 5 would increase funding to Michigan public schools, colleges and universities; reduce funding differences between districts; and shift part of the costs of school employee pensions from local districts to the state. Before analyzing Proposal 5, it is worth reviewing what has actually happened to education funding and school employee pension liabilities in the years since Proposal A went into effect. These areas are discussed in turn below.

Both the funding of Michigan school districts and the overall state budget underwent a major restructuring after 1994, when the passage of Proposal A shifted much of the responsibility for financing primary and secondary public education from local property taxes levied by public school districts to sales and property taxes levied by the state.

Since 1995, the Michigan economy and the state budget have experienced a roller-coaster ride of prosperity and decline. These trends have had a pronounced impact on the state government’s "general fund," which is the main source of discretionary tax revenue used to finance part or all of a number of state programs, including state universities and community colleges.† Proposal 5 would require the general fund to finance the proposal’s mandated additional education spending. Taxes placed in the general fund include all or part of the Single Business Tax; personal income taxes; the state sales tax; cigarette and alcohol taxes; and a variety of other specialized taxes.

From 1995 to 2000, a strong state and national economy led to large tax revenues for the general fund. Annual spending from the general fund was almost 18 percent higher in 2000 than it was in 1995, comfortably outpacing total inflation for the period.

This trend reversed abruptly after the 2001 national recession. The loss of jobs and the flight of capital from Michigan between 2001 and 2005 resulted in a substantial decline in tax collection, affecting spending for many state programs. Had general fund revenue from 2001 to 2005 kept pace with inflation, it would have been about $1 billion higher in 2005 than it was in 2001. Instead, general fund revenue was more than $1 billion lower than it was in 2001 — a decline of nearly 11 percent.[7]

The general fund is the source for state spending on community colleges and universities, and the fund sometimes supplements state spending on primary and secondary schools (see "Local School District Funding After Proposal A" below). The impact of the general fund revenues on state education spending is one impetus for the drafting and submission of Proposal 5. The K-16 Coalition, the primary political sponsor of Proposal 5, has noted on its Web site, "For the last three years, K-12 school districts saw no increase in State Aid and Michigan’s community colleges and universities had budgets slashed 15%."[8]‡ The language of Proposal 5 would prevent the state Legislature from making such decisions — an outcome that involves trade-offs that will be analyzed below under "Analysis of Proposal 5: Budget Effects."

|

† Most public school education money is provided by the state’s school aid fund, which is financed partly by a constitutionally dedicated portion of state sales and property taxes. |

|

‡The Web site was later updated, and the language was changed to read, “In school years 2001-2002, 2002-2003 and 2003-2004, K-12 schools received no increase in State Aid and Michigan’s community colleges and universities had budgets slashed 15%.” The years cited do not appear to correspond to the fiscal years in which state aid to primary and secondary schools essentially remained flat. As indicated in the text of this study, the three years in which funding remained effectively unchanged were fiscal 2003, 2004 and 2005. Regardless, the statement is essentially true. |

The major budget source for state primary and secondary education spending is the state’s "school aid fund." Since the advent of Proposal A, the monies in this fund have typically comprised at least 90 percent of the state’s spending on primary and secondary education, with any additional spending coming from the state’s general fund.

Since passage of Proposal A, the aggregate annual state funding for local schools has grown faster than the rate of inflation. State school aid fund spending in 2005 would have been 27 percent higher than in 1995 if spending had increased only at the inflation rate; in actuality, state school aid fund spending in 2005 was more than 40 percent higher than in 1995 — about $1 billion above the inflation rate.[9]

Within that decade, there have been years in which the growth in annual state spending on local schools fell to essentially zero (and in one year, very slightly below zero). Like the general fund, the school aid fund did not keep pace with inflation from 2001 through 2005, the period in which the national recession drove a decline in tax revenues. As suggested above, the state’s basic per-pupil foundation allowance to local school districts remained substantially unchanged in fiscal 2003, 2004 and 2005.

Michigan’s public universities and community colleges have the constitutional authority autonomously to raise money from tuition and other sources. Unlike public school districts, higher education institutions derive more funding from tuition and other sources than they do from direct state government aid. Almost all of the state aid that public universities and community colleges do receive comes from the general fund budget. Appropriations to support the state’s universities constitute nearly 21 percent of the state’s general fund expenditures.

Prior to the sharp decline in general fund tax revenue after 2001, state spending on community colleges and universities increased significantly. Taken together, state appropriations for community colleges and universities were nearly 37 percent higher in 2001 than in 1995, while inflation increased by about 15 percent during the same period. Spending for higher education in Michigan was also high relative to other states: According to the Nelson A. Rockefeller Institute of Government Fiscal Studies Program, spending per capita by Michigan’s public institutions of higher education ranked ninth highest in the nation for 2002 — nearly 33 percent above the national average.[10]

State funding of higher education was reduced, however, following the post-2001 decrease in state general fund revenues. State higher education expenditures in 2005 were nearly 10 percent lower than they had been in 2001. As will be discussed below, this reduction was not quite as large as the overall decline in general fund tax revenues.

In a comprehensive 2004 report, "Financing Michigan Retired Teacher Pension and Health Care Benefits," the nonprofit Citizens Research Council of Michigan predicted that the annual contribution rate paid by local school districts into MPSERS would increase from 14.87 percent of payroll in 2005 to 32 percent by 2020.[11] The CRC projection is both plausible and widely accepted, even though the school districts’ MPSERS contribution rate has fluctuated at or below 15 percent for more than a decade.

Several reasons account for the projected hike. Some of the projected cost increase is due to a disproportionately large number of retirees entering the system, while some arises from the need to make up for recent stock market losses. Another major factor is a substantial projected increase in the cost of retiree health care benefits. While the retiree health care benefit represented less than 45 percent of MPSERS costs in 2005, the CRC report predicted that it will account for more than 62 percent of total costs in 2020.[12]

The financial implications are troubling. The increases in the MPSERS contribution rate have already begun to consume a large percentage of each additional dollar sent to Michigan’s public school districts. The Michigan Senate Fiscal Agency calculates that the total retirement fund contribution increases from 2004 through 2006 cost the average school district an additional $178 per pupil, exceeding the state’s per-pupil foundation allowance increase during the period by $3 per pupil.[13]

The Michigan Senate Fiscal Agency estimates the MPSERS contribution rate will be 17.74 percent in the 2006-2007 school year. These rates would be the highest ever paid since local schools assumed cost obligation for MPSERS, even though the MSFA estimates are about 1 percentage point lower than the CRC’s projections. If the actual MPSERS rate increases remain within 1 percentage point of the CRC’s estimates for the next 10 years, MPSERS contribution costs will increase more than 94 percent by 2016. In contrast, the MPSERS contribution cost increase from 1996 to 2006 was about 50 percent.[14]±

The MSFA’s estimates tend to confirm the CRC projection of a steep upward climb in MPSERS contribution rates in coming decades. Absent unprecedented increases in state aid for local school districts, there is a significant possibility that MPSERS spending will consume nearly all of each additional taxpayer dollar taken for local schools over this time and possibly much more. Assessing the implications of its prediction, the Citizens Research Council stated: "The outlook for MPSERS contributions and the effect on school district budgets is decidedly gloomy."[15]

Concern over the impact on school districts appears to be a significant reason that supporters of Proposal 5 would like to shift responsibility for prospective MPSERS hikes from school districts to state government. For instance, Tom White, current chair of the K-16 Coalition and executive director of the Michigan Association of School Business Officers, was recently quoted in the Detroit Free Press addressing the MPSERS cost issue: "This is killing us. We could be spending $1,200 per pupil on retirement costs by 2008." He added, "We have to begin addressing these costs."[16]

Indeed, these costs will need to be addressed. As discussed below, however, transferring partial responsibility for MPSERS contributions to the state is not likely to achieve the goal of cost containment.

|

± The Citizens Research Council assumes 2 percent annual growth through 2016 in the wage base on which MPSERS contributions are calculated. This projection employs the same assumption. Estimated contribution rates from 2008 through 2016 are the CRC estimates minus 1 percentage point. Historical MPSERS data are taken from the Michigan Senate Fiscal Agency. |

Primary and Secondary Education

As noted above, supporters of Proposal 5 have cited recent declines in education funding. A comment on the K-16 Coalition Web site notes, "For the last three years, K-12 school districts saw no increase in State Aid. ..."[17]

State government spending on primary and secondary education has indeed remained flat during most of Michigan’s recession, a period during which general fund revenues declined substantially in both real and nominal terms. This lack of funding growth did contribute to fiscal challenges for school districts.

Nevertheless, the recession’s effect on state funding for primary and secondary education has not been as large as it has been for most other state programs. Fiscal 2005 general fund spending for many general fund-reliant programs, including economic development programs and the department of civil rights, was down significantly from 2001 levels.

In contrast, school aid fund spending in fiscal 2005 was about the same as — and in fact, slightly higher than — it was in 2001. As recently as fiscal 2002, the basic per-pupil foundation allowance increased more than 8 percent from the year before,[18] and another per-pupil increase of about $200 has been budgeted for fiscal 2007.[19]

The relative advantage that primary and secondary spending had over other program budgets might seem unusual, given that primary and secondary education is the state’s single largest budget item and that small percentage cuts in this spending area would have yielded relatively large savings. These savings probably would have been welcome at a time of lower revenues, rising taxes and substantial state spending reductions. The Michigan Constitution, however, dedicates certain sales and property taxes to education. These tax revenues, which did not decline as rapidly as the revenues placed in the general fund, were spent on primary and secondary schooling during the years in question.

The more generous treatment of state primary and secondary spending helped ensure that Michigan’s per-capita spending on primary and secondary education would remain high relative to long-term inflation and relative to other states. As noted above in "Local School District Funding After Proposal A," aggregate annual state funding for local schools from fiscal 1995 to fiscal 2005 increased by more than 40 percent, compared to a total inflation rate of 27 percent.

Michigan is still one of the highest-spending states on public primary and secondary education. According to the federal government’s National Center for Education Statistics, Michigan’s total per-pupil spending in 2003 was ninth in the nation,[20] and according to the National Education Association, the average salary for Michigan instructional staff was eighth.[21]

The American Legislative Exchange Council reports similar findings, writing that Michigan’s per-pupil spending in 2004 was ninth among the states and nearly 15 percent above the national average, while the average compensation for instructional staff at Michigan public schools that year was more than $54,000 — second-highest in the nation, and more than 25 percent above the national average.[22] The NEA, in contrast, estimated Michigan’s compensation for instructional staff to be the eighth-highest among the states, but also concluded that this compensation exceeded $54,000.[23] Michigan’s school spending ranked similarly in previous years.[24]

While state spending growth on primary and secondary education has slowed during the recent recession, school funding during the past decade has risen significantly above the rate of inflation, and this funding has remained high in comparison to other states. If one of Proposal 5’s main goals is to ensure high and rising primary and secondary school spending over the long term, it would seem that goal has already been met.

Michigan’s state community colleges and universities have had high spending rates compared to public higher education institutions in other states. As noted earlier, spending per capita by Michigan’s public institutions of higher education was ninth in the nation in 2002 — nearly 33 percent above the national average.[25]

State funding for community colleges and universities has changed more during the current recession than has state funding for primary and secondary education. State aid to community colleges and universities in fiscal 2005 was nearly 10 percent lower than in fiscal 2001.

Nonetheless, this cut was less than the nearly 11 percent decline in general fund revenues. Some other state programs, such as the state "strategic fund" (for "economic development"), were cut significantly more.[26]

It is perhaps unsurprising that the governor and the Legislature cut state aid to universities and community colleges, rather than school districts. Universities and community colleges have other sources of nonstate revenue, including tuition. It is clear in retrospect that these institutions were generally able to tap these other sources to compensate for the lower levels of state funding. Total expenditures from the general funds of the four-year universities increased every single year from 2001 thru 2005, even as aid to these schools from the state general fund was reduced.[27]

To help achieve this increased spending, the universities raised the average in-state undergraduate tuition rate during this period by nearly 38 percent, while total inflation for the same period was just above 10 percent.[28] In arguing for Proposal 5, the K-16 Coalition has pointed to this trend, observing that the reduction in state aid to colleges has led to an increase in college tuition.[29]

There appears to be some truth in this observation, but it is worth noting that large tuition hikes were common before the reductions in direct state aid. From 1995 through 2001, while state appropriations for universities increased faster than the rate of inflation, tuition did as well. Average in-state tuition at Michigan universities was more than 28 percent higher in 2001 than it had been in 1995 — an increase of nearly twice the inflation rate, which was a little more than 15 percent for the period.[30]

Thus, while Proposal 5 might ameliorate tuition hikes during years when state government revenue growth declines, the problem of rapidly rising tuition at state colleges and universities is unlikely to be solved even if Proposal 5 passes. Indeed, given the recent record of state aid and tuition, large annual tuition hikes seem likely to persist even if state government provides the accelerated rate of state aid growth that the governor and Legislature furnished from 1995 to 2001, when Michigan’s economy was strong.

Had Proposal 5’s requirements been in effect in recent years, state spending for primary and secondary education would have had to increase in fiscal 2003, 2004 and 2005, rather than remain essentially constant. Proposal 5’s effect on spending for universities and community colleges would have been even larger. Rather than declining, higher education spending would have had to increase at the 10 percent inflation rate for that period, producing state spending in 2005 that was $233 million above 2001.[31]

Accommodating such budget increases for a major spending area like education would have demanded significant amounts of money. Finding these sums would have been even more difficult during the recession-induced decline in state tax revenue, which left 2005 general fund spending more than $1 billion below that of 2001. Programs that received large cuts might have received larger ones, or taxes might have been raised even further during the recession.

Without Proposal 5’s spending requirements, lawmakers had the discretion to cut some programs more than others, shielding some programs from the full impact of the revenue decline. For example, from 2001 to 2005, state spending on education at all levels did not drop as much as revenue for the general fund did. State spending for prisons was even slightly higher in 2005 than in 2001, while general fund money spent on the state police dropped by more than 24 percent.[32] (Note that much of this decline in state funding for the state police was offset by increased funds from other sources, such as federal monies.[33])

If Proposal 5 were to pass, state lawmakers would have much less discretion during any future decline in state revenue growth. Taken together, the Proposal 5 education spending areas are about 54 percent of state revenue from state sources. By mandating that public education spending rise with the rate of inflation, Proposal 5 would require increases for this 54 percent, regardless of the economic condition of the state and the funds available for the remaining 46 percent.[34] State lawmakers would find it hard to balance the budget (a constitutional requirement in Michigan) without raising taxes or making reductions in state spending for human services, corrections, veterans services or other state programs receiving general fund revenue.

Potential Reductions in Certain State Education Spending in Fiscal 2007 as a Result of Proposal 5

Some of the state programs that would likely face budget pressure are education programs that are not specifically protected by Proposal 5. As explained above in "Overview and Background of Proposal 5: Provisions," Proposal 5 requires at least an annual inflationary increase in global state education spending, as well as similar annual increases in a number of specific education spending areas, such as the primary and secondary school foundation allowance.

Certain primary and secondary education areas, however, are not required to increase at all and could freely decrease, as long as overall education spending rose at no less than the inflation rate (a list of these "unprotected" areas appears in Graphic 5). These unprotected education areas would in fact be at risk of losing state funding.

The reason involves the nature of the protected spending categories. It is possible, for instance, to meet Proposal 5’s inflationary mandate for total school aid spending without satisfying the proposal’s mandate for inflationary increases in the per-pupil foundation allowance. An inflationary increase in total per-pupil foundation allowance spending might not provide an inflationary increase in the foundation allowance itself if the number of students were to increase or if there were a net increase in the number of students at higher-spending schools. In this case, lawmakers would need more money to meet the proposal’s requirement for an inflationary increase in the per-pupil foundation allowance.

At this point, the presence of "protected" and "unprotected" education spending would produce a significant incentive for lawmakers to shift funds from unprotected areas to protected ones. Such shifts would not decrease overall education spending, and they would enable lawmakers in the first year to avoid raising taxes or cutting more noneducation areas in order to meet the inflationary increases required for the per-pupil education areas — such as the foundation allowance — specifically shielded by Proposal 5.

|

Status of Education Spending Areas |

|

“Protected”: Must Increase |

|

Primary and Secondary Per-Pupil “At-Risk” Pupil Spending Special Education Spending Intermediate School District Operations Spending |

|

“Unprotected”: No Requirement That Spending in |

|

Adult Education Bus Driver Safety Instruction and Bus Inspections

School Readiness Program (preschool programs for Children of Incarcerated Parents Math/Science Centers School Breakfast Programs Vocational Education Hearing and Vision Screening

Engineering Michigan’s Future Juvenile Detention Facility Programs Court-Placed Pupils Adolescent Health Centers |

Indeed, a recent budget memorandum by the Michigan Senate Fiscal Agency suggests that state government would in fact reduce spending in unprotected education areas in fiscal 2007, the first year in which the proposal would take effect. According to the memorandum, the mandatory general fund costs of Proposal 5 in the first year of implementation would exceed the recently enacted appropriations for the fiscal 2007 general fund budget by $566.6 million.[36] This working figure is one of the report’s major findings. In fact, $565 million has become the estimated cost of the proposal used in the official description of Proposal 5 on the November ballot.

Yet $566.6 million is not the full estimated cost of Proposal 5; rather, it is the cost calculated by the MSFA on the assumption that "unprotected" education spending areas would be tapped to provide $141.7 million in monies for Proposal 5’s protected education spending areas. This assumption is explained in a note in the analysis:

"Note: The Legislature’s increase in gross baseline funding for K-12, combined with the dollars available in ‘discretionary’ or ‘nonrequired’ categoricals appropriated in the Legislature’s K-12 budget would provide sufficient funding to pay for the specific funding ‘guarantees’ listed above provided that some of the existing School Aid discretionary categoricals were reduced from their Conference report FY 2006-07 level and new items in the Legislature’s budget were not funded. In other words, existing and new program funds (e.g., Adult Education, School Readiness, or Middle School Math grants) could be used to offset the costs found in the specific funding guarantees required in the initiative. However, if the K-16 costs were simply added on top of the Legislature’s School Aid budget, then the costs of funding all of the Legislature’s initiatives plus the K-16 requirements would be $141.7 million more than the $180.3 million noted above, or $322.0 million."[37] (Emphasis in original.)

The MSFA therefore effectively estimates Proposal 5’s total first-year cost, including the proposal’s MPSERS costs, to be $708.3 million. Since $708.3 million would place pressure on the state budget at a time when Michigan’s economy and state revenues continue to lag, it is not unreasonable to assume, as the MSFA does, that lawmakers would respond to Proposal 5 by shifting funds away from "unprotected" education areas. This assumption seems particularly valid given that lawmakers have made cuts to these programs in recent years. Even with the offsets, the remaining $566.6 million would represent a hike of 9 percent over the 2006 spending level — more than double the estimated rate of inflation from 2006 to 2007.

Of course, local districts could choose to use the extra money provided to them by Proposal 5 to replace any lost state monies for these specific programs. In addition, cuts to these "unprotected" state programs may well be justified; the Mackinac Center, for instance, has recommended reductions in state spending on school readiness grants.

Potential Reductions in Noneducation Spending as a Result of Proposal 5

If "unprotected" education spending were not tapped to increase funding for Proposal 5’s protected education areas, state lawmakers would be even more likely to consider cuts in noneducation spending. This approach would indeed shift state spending priorities even further toward education — Proposal 5’s ostensible purpose — but a first-year shift of up to $708.3 million dollars from noneducation spending would indeed be significant. (Tax increases to supplement revenue are considered below, in "Potential Tax Increases as a Result of Proposal 5.")

Such a shift would come almost exclusively from the state’s general fund monies. Some of these funds would not be available under Proposal 5: In fiscal 2007, about 21 percent of the general fund budget will be spent on community colleges and universities, a spending area that would have to increase at no less than the inflation rate.[38] In addition, nearly 1 percent of the general fund will be dedicated to the state’s contractual commitments, such as building rent and debt payment, some of which is education-related. (This spending cannot legally be decreased.)[39]

Thus, at least 22 percent of the general fund would not be available to buttress education spending. If lawmakers chose to raise the revenue required by Proposal 5 in fiscal 2007 through noneducation spending cuts, the remaining budgets receiving general fund money would bear the brunt. The $708.3 million needed to meet Proposal 5’s education spending requirements would represent 9.8 percent of the remaining noneducation general fund spending.[40] The $566.6 million that would be needed if "unprotected" education spending were also cut would represent 7.9 percent.[41]

Hence, assuming no increase in taxes, the governor and the Legislature could raise enough revenue to meet Proposal 5’s spending requirements in one of two ways: by making a 9.8 percent cut to noneducation general fund spending; or by making a 7.9 percent cut to noneducation general fund spending and $141.7 million in cuts to "unprotected" primary and secondary education spending. These cuts could be made to each program across the board. Alternatively, some budgets could be cut more than others, but most budget areas simply are not large enough to provide a significant percentage of the money needed. For instance, the combined general fund expenditures to maintain the office of the governor, the state Legislature and the state judiciary are less than half of the $566.6 million dollars that would be needed at minimum. The only noneducation general fund budgets large enough to receive the full brunt of such spending are corrections, human services and community health.

Corrections. Nearly the entire state prison budget is paid from the general fund. If all of the spending required for Proposal 5 came from the corrections budget, the $708.3 million in extra spending would represent 36 percent of fiscal 2007 total prison spending; $566.6 million would represent about 29 percent.

Human Services. The state’s primary poverty assistance program (welfare) relies on the general fund for one-quarter of its spending. If all of the spending required for Proposal 5 came from the human services budget, the $708.3 million in extra spending would be equivalent to 16 percent of the total fiscal 2007 human services budget; $566.6 million would represent almost 13 percent.

Community Health. This program delivers assistance to public hospitals; Medicaid funding for those with limited incomes; and assistance for those with mental illnesses and developmental disabilities. Community health is by far the largest program receiving general fund money, and the general fund provides one-quarter of all community health funding. If all of the spending required for Proposal 5 in fiscal 2007 came from community health, the $708.3 million in education spending would be equivalent to more than 6 percent of the total community health budget, or about 24 percent of community health’s general fund revenues. Similarly, $566.6 million would be equivalent to about 5 percent of the total community health budget, or 19 percent of community health’s general fund revenues.

Potential Tax Increases as a Result of Proposal 5

Substantial tax increases could also be used to raise some or all of the first-year spending required by Proposal 5. Just as this money represented a significant percentage of general spending, however, this sum could also represent a significant increase in taxes.

For instance, $708.3 million would represent more than 37 percent of the revenue currently raised by the Single Business Tax, the state’s main source of business income taxation; $566.6 million would represent more than 30 percent.[42] It is also probable that increases of 30 percent to 37 percent in the SBT would not be sufficient to increase SBT revenues by like amounts, particularly during an economic slump. An SBT tax increase could instead depress the state’s business activity, producing lower-than-expected tax revenues.

In addition, the Single Business Tax is high compared to the corporate income taxes imposed by other states. Michigan’s Single Business Tax was ranked the second-worst business tax in America by the nonpartisan Tax Foundation of Washington, D.C.[43] The Foundation warned in March 2006 that this tax could cause Michigan to lose jobs to neighboring Indiana.[44]

Given that the Legislature has recently approved an end to the SBT effective Dec. 31, 2007, lawmakers may consider raising revenue for Proposal 5’s mandates by increasing taxes paid directly by Michigan’s citizens. In the case of the sales tax, the estimated $708.3 million cost of Proposal 5 in fiscal 2007 would represent 8.4 percent of revenue, while $566.6 million would represent 6.7 percent.[45] The sales tax rate cannot be raised above its current level of 6 percent without amending the Michigan Constitution,** but sales tax revenue could be increased by broadening the base of the tax to include services and other industries whose sales are currently untaxed.

In the case of the income tax, $708.3 million would represent about 11.1 percent of current revenue, while $566.6 million would represent 8.9 percent.[46] As with the SBT, the sales and income taxes would probably have to be increased by more than these percentages to net the requisite revenue, since increases in tax rates can deter the activity subject to the tax and therefore net less revenue than a simple proportional estimate would suggest.

Raising these taxes would likely have economic costs, however. Raising taxes on Michigan households would decrease their disposable income at a time of relatively high state unemployment, while raising the effective cost of such things as higher education. This result would tend to counter one of the intended goals of Proposal 5, which, according to the K-16 Coalition, is to make college more affordable.[47]

|

** The state sales tax rate is limited by Article 9 Section 8 of the state constitution. |

Colorado’s Experience With a Similar Law

In November 2000, Colorado voters narrowly ratified Amendment 23, which placed a state education spending mandate in the Colorado Constitution. The amendment required that during the 10 years following its approval, state spending on local public schools increase annually by no less than one percentage point above the rate of inflation. In subsequent years, the amendment required state spending on local public schools to increase at or above the inflation rate.

When Colorado taxpayers voted to approve Amendment 23, the state was experiencing annual state budget surpluses of nearly $1 billion. Under a requirement in the Colorado Constitution, these surpluses were being refunded to taxpayers as checks from the state government. A later study by the Colorado General Assembly summarized the budget environment of the day by stating, "It was widely believed that the state’s surplus had grown so large that an economic downturn would not eliminate it."[48]

Unfortunately, a recession began as the spending mandate was implemented, and the budget surpluses ended. By 2005, state tax collections were running more than $200 million less than they had been in 2001.

In the interim, Amendment 23’s spending mandate had pressed the state’s primary and secondary education spending up $719 million.[49] Faced with a nearly billion-dollar discrepancy between its previous revenues and its currently mandated costs, Colorado lawmakers made disproportionate cuts to popular state programs, such as capital construction and homestead property tax exemptions for seniors.[50] In 2005, with the state coming out of recession and budget experts again projecting surpluses, advocates of the programs that had been cut helped pass Referendum C, a spending mandate that will allow the state to keep all of the projected revenue surpluses for the next five years, rather than return them as taxpayer refunds.

Colorado’s experience suggests that tax increases, spending cuts to noneducation programs, or both are reasonably likely when state government responds to mandated education spending increases. True, Amendment 23’s "inflation-plus-one" requirement is more demanding than the inflationary increase required by Proposal 5. Still, the requirements of Michigan’s Proposal 5 would be broader than Colorado’s Amendment 23, since Proposal 5 includes additional specific education spending guarantees and requires inflationary spending increases for higher education, not just primary and secondary schooling.

The spending pressures faced by the Colorado General Assembly were probably no more severe than those that would be faced by the Michigan Legislature under Proposal 5. The reductions in spending for noneducation programs in Colorado during the state’s recession were substantial, so much so that these cuts were unpopular enough to convince a majority of Colorado voters to suspend future tax refunds in 2005. Referendum C’s five-year suspension of these refunds, in turn, amounted to a de facto total state tax increase estimated to exceed $4.88 billion, according to a recent press report.[51]

The Additional Liability of MPSERS

Most of the public attention to Proposal 5 has involved the provisions for inflationary education spending increases. The proposal’s provision for the MPSERS cost transfer deserves serious attention, however, because this provision would account for more than half of the projected cost increase in fiscal 2007 if Proposal 5 were approved.

Proposal 5’s MPSERS provision does not attempt to address MPSERS spending by changing its cost structure, though such changes have been recommended by others. For instance, the Citizens Research Council has suggested that MPSERS spending might be brought under control by lowering pension benefits for new hires, reducing MPSERS health care benefits for employees with less than 30 years vested in the system and requiring higher school employee payments for both pension and health care benefits. The Dec. 14, 2004, Detroit Free Press reported that Tom White, executive director of the Michigan Association of School Business Officers and chairman of the K-16 Coalition, has suggested that providing only a partial MPSERS health benefit to school employees with less than 30 years’ employment could help reduce future costs.[52]

Proposal 5, however, focuses on transferring MPSERS costs from district budgets to the state budget whenever they exceed a certain level (essentially 14.87 percent of payroll, if costs rise as predicted in the next two years). The MPSERS provision is written in a way that would prevent the state from counting its MPSERS payments towards the education spending mandated by Proposal 5.

Placing MPSERS outside the state’s education budget would have two effects on the state budget. First, it would raise the overall state liability for funding various aspects of state education programs. This liability would include not just paying an inflationary increase in education spending as defined under the proposal, but also paying certain MPSERS benefits in addition, since the MPSERS benefits could no longer be counted as part of the inflationary education spending increase mandated by the proposal. This added fiscal responsibility is one reason that the first-year cost of Proposal 5 would be estimated to reach $708.3 million if no funds are transferred from "unprotected" to "protected" education programs.

Second, the provision further reduces the amount of state noneducation spending that would remain discretionary under Proposal 5. This constraint would become significant whenever revenues were scarce and lawmakers chose to find money for Proposal 5’s spending mandates by reducing budgets for noneducation programs. Since MPSERS costs would effectively be protected "noneducation" spending, larger percentage cuts would be necessary to other noneducation programs (such as state police, welfare, environmental quality or community health) in order to raise the same amount of money.

The state’s MPSERS responsibility under Proposal 5 would amount to a significant portion of protected "noneducation" spending. If Proposal 5 were to pass, the state general fund budget would assume responsibility for $386.3 million of an estimated $1.9 billion total MPSERS cost in fiscal 2007. This MPSERS cost is projected to increase considerably, but $386.3 million is in fact larger than 16 of the 26 fiscal 2006 departmental budgets.[53] Proposal 5’s MPSERS provision would therefore significantly increase the stakes in state budget decisions during slowdowns in revenue, such as the current one.

Arguably, this pressure could increase state government’s incentives to reform MPSERS by adjusting its benefits to a more sustainable level. But it may also encourage distorted spending decisions by local school districts, as discussed below.

Potential Distortions in School District Staff Decisions

By putting the financial pressure of rising MPSERS costs on state government, Proposal 5’s MPSERS provision would relieve school districts of the need to manage rising MPSERS payments — an outcome that would make local budgeting easier, but would subsidize school districts’ personnel budgets by reducing the local cost of payroll. This subsidy in turn could lead districts to retain or hire staff that the districts could not otherwise afford.

Some may view such subsidies as inherently good, since they can result in more school personnel. These personnel are not always teachers or classroom employees, however; some may be service employees or administrators who are not necessarily critical to classroom learning. In addition, subsidies to hire and retain personnel can distort budget decisions in ways that cause difficulties later. The Detroit Public Schools amassed a $200 million deficit in 2004 following a period in which it increased its staff while student enrollment was falling significantly. It seems unlikely that even Proposal 5’s compensation for districts with declining enrollment could have made such a strategy viable in the long run.[54]

The MPSERS subsidy included in Proposal 5 would also remove an additional incentive for school boards to bargain carefully with employee unions over wages and salaries. By the nature of MPSERS’ defined-benefit plan, any raises that school officials award lead directly to proportional increases in MPSERS costs. Under the current system, both these MPSERS cost increases and the pay raises must be financed by the school district, meaning it assumes the full cost of its payroll decisions.

This fiduciary responsibility provides school boards with a substantial financial incentive to keep salaries and wages from rising out of control. Consider a school district with a $10 million payroll. At present, that school district is financing this payroll and a MPSERS contribution equal to 14.87 percent of this payroll (about $1.5 million). With projections of the MPSERS contribution rising to 17 percent of payroll next year, the district is already planning on a big cost increase — around $213,000 — even if payroll doesn’t rise at all. The district is therefore already likely to be careful about adding to its payroll; every dollar it grants in new wages will bring the district an additional 17 cents in new retirement costs — or, in a few years, 20 cents or 25 cents, if the MPSERS contribution rate continues to rise as expected.

In contrast, if Proposal 5 passes, school districts will be paying 14.87 percent of payroll or less. The district described above would not need to cover the $213,000 spending increase that would occur due to the rise in the MPSERS contribution rate. This de facto state subsidy could encourage the school board to use any of the district’s remaining money for new hires, further pay hikes or retaining personnel that the district could not otherwise afford. Part of any additional MPSERS contribution occasioned by the district’s subsequent payroll decision would be paid not by the district, but by the state. The state, in turn, would have no immediate means of restraining the spending, except to send less money to the district in the first place — an approach limited by Proposal 5’s other education spending mandates.

The partial division between payroll decisions and those who pay for them could lead to a further acceleration of MPSERS costs. The resulting dynamic would be similar to the "third-party payer" dilemma in health care.

Concern Over Adequate Funding for MPSERS

Proposal 5’s MPSERS provision would move increases in MPSERS costs into the state’s general fund, where higher costs are not as large a percentage of the budget’s total spending as they are of school districts’ total spending. Because the state must still find money to finance MPSERS costs, the shift to a larger budget is still unlikely to end pressure to reform MPSERS. To the extent that the budgeting shift stalled reform of the MPSERS system, however, the cost to state taxpayers would be higher.

It is possible to argue that these higher costs are worthwhile. In December 2004, the Detroit Free Press quoted a Michigan Education Association spokeswoman referring to MPSERS benefits as saying, "It’s a reasonable package that attracts people to the profession in the first place. … Any reduction in benefits hurts our ability to recruit."[55]

There may indeed be recruiting trade-offs in restraining MPSERS health and retirement benefits for future employees. But benchmarking MPSERS benefits for school employees with the retirement benefits provided by other employers suggests that the school employees’ package is unusually generous.

According to a survey of American employers by the Kaiser Family Foundation, just 34 percent of firms with 200 or more employees provided health care benefits to retirees. Among private firms and small businesses with fewer than 200 employees, just 3 percent offered such a benefit. The substantial majority of private-sector employers do not offer any retirement health care benefit at all.[56]

Similarly, a majority of workers do not receive a defined-benefit pension comparable to MPSERS. Recent estimates suggest that fewer than half of American workers receive retirement savings plans from their employer, and that the majority of those who do have a 401(k) or other defined-contribution plan.[57] These defined-contribution plans do not guarantee a certain pension payment, but rather provide tax-favored retiremement savings.

Even public-sector employers have converted to defined-contribution plans. For example, Michigan judges, legislators and most other state employees were switched to defined-contribution plans in the late 1990s. Public school teachers were ultimately not included in this change. MPSERS itself recognizes that its pension program is generous; a MPSERS Web page greets school employees with the message: "Welcome! As a member of Michigan’s Public School Employees Retirement System, you are eligible for one of the best public pensions around."[58]

Most Michigan businesses and their employees are paying taxes to support a MPSERS benefit that is considerably better than the retirement plan that is available to them. At the same time, the assertions made in the Citizens Research Council report on MPSERS have not been credibly refuted since their release, and they have been reasonably accurate so far. The CRC report portrays a serious financial challenge for the taxpayers of Michigan that will grow substantially larger and more difficult to remedy with each passing year that it remains unaddressed.

State spending on education is often seen as an investment in more highly educated citizens and a better economy. The K-16 Coalition has suggested such benefits from Proposal 5, having written on the coalition’s Web site: "This proposal lays the foundation for increased student achievement. Well-funded districts are better equipped to provide maximum opportunity for student achievement."[59] The Web site also argues: "The proposal will create jobs. By making a steady investment in education now, this proposal will lay the foundation for economic growth and job creation and help Michigan compete globally for high-tech and other jobs."[60]

As recounted above in "Assessing Previous Levels of Education Funding," Michigan has engaged in some of the nation’s highest spending on local school districts and higher education. In 1984, 1994 and 2004, per-pupil spending by Michigan public schools ranked in the top 10 states; average teacher compensation was in the top five; and spending by Michigan’s colleges and universities in 2002 was ninth in the nation.[61]

However, in 2003 Michigan eighth-graders ranked 34th and 27th in the nation on national tests for math and reading, respectively; in 2005, they ranked 34th and 29th.[62] And Michigan’s economy has remained one of the worst ever since, steadily losing jobs while the rest of the nation has been adding them. There does not seem to be a correlation between Michigan’s increased spending for education on the one hand and brighter kids and more jobs on the other.[63]

Indeed, economist Richard Vedder researched the relationship between economic growth and state spending on universities, and he published his findings in a 2004 book entitled, "Going Broke by Degree: Why College Costs Too Much." Describing that research, Vedder has written: "I found a strong negative relationship — higher state spending equals lower rates of economic growth. At the very minimum, the rate of return on state government investments in higher education is very low and very possibly negative at the margin."[64]

Proposal 5, however, could lead to unintended economic effects. To the extent that Michigan lawmakers feel compelled to increase or maintain Michigan’s current tax burden in order to meet Proposal 5’s spending mandates, the state’s business climate could actually be harmed. The Tax Foundation has found not only that Michigan’s Single Business Tax imposes the second-heaviest tax burden in the nation,[65] but also that Michigan’s overall state and local tax burden in 2006 is 16th highest in the nation.[66] Neither of these figures suggests a tax climate likely to improve Michigan’s weak economy.

The proposal could also produce unintended educational effects. Consider Proposal 5’s provision to grant per-pupil foundation allowances to districts with declining enrollment based not on the district’s current enrollment, but on a three-year average that includes the previous two years’ enrollments. This provision could insulate poorly performing districts from the consequences of their failures by providing them with more money than they would otherwise receive. This reduced penalty could lower their incentive to reform.††

It is true that some comparatively desirable school districts in Michigan exist in communities that have, for economic or other noneducational reasons, declining student populations. These districts, however, can demonstrate — and often have demonstrated — that they are desirable by successfully attracting students from other districts through the state’s public school choice program. The money these districts receive for their "school of choice" students helps offset the money they have lost through their local enrollment decline.

The opportunity to regain students through this school choice dynamic is, under the state’s present school choice system, less likely to be available to the sparsely populated, often out-of-the-way districts that are currently permitted to use the three-year average for state reimbursement. Whatever the wisdom of the three-year formula for these districts, extending the option to all districts risks maintaining support to school institutions independent of the needs they serve.

|

†† It is true that in fiscal 2007, state lawmakers began extending additional monies to districts with declining enrollment, thereby removing some of a district’s incentive to improve. Proposal 5’s formula, however, would generally grant a district an even larger sum of money and therefore a larger disincentive. In addition, overturning the proposal’s formula for districts with a declining student population would take a three fourths vote of both branches of the state Legislature, making the provision much harder to repeal than the fiscal 2007 payment. |

Districts with declining enrollment in today’s increased public school choice environment are losing money largely because they are failing to compete successfully for students. Proposal 5’s new spending for such districts could mean that the worst-performing districts are encouraged to postpone restructuring. The incentive to reform would be further softened by the proposal’s mandated inflationary increases in education spending, since this per-pupil funding growth would occur regardless of academic performance.

The major findings of this study appear in the "Executive Summary." They suggest several conclusions.

State spending on primary, secondary and higher education has been affected by Michigan’s current recession. Nevertheless, state lawmakers have protected education at all levels from the full consequences of the revenue decline. State spending on primary and secondary education even increased slightly during this period, while state colleges and universities were able to support their spending by supplementing their reduced state monies with tuition increases and funds from other sources.

Michigan has maintained its long-term practice of generous state education spending. From 1995 to 2005, state education spending, which was already high compared to the national average, has grown generously — well above the inflation rate. Proposal 5 does not appear necessary to ensure high and rising education spending over the long term.

In the short term Proposal 5 could produce results unanticipated by voters. The proposal mandates could lead to first-year reductions in state spending for certain education areas. In addition, the proposal could lead to cuts in major noneducation programs or to higher taxes. These last two pressures would likely recur with each state recession.

The largest single portion of Proposal 5’s estimated cost is related to MPSERS: $386.3 million of the projected $566.6 million (or $708.3 million) cost in fiscal 2007. As presently structured, MPSERS will cost taxpayers substantial and growing sums of money in coming decades. The MPSERS benefit has few rivals in the marketplace. Some private- and public-sector employers facing comparable pension problems have modernized the plans to make the benefits financially sustainable and sufficiently flexible to attract mobile professionals in the contemporary marketplace.

Such restructuring would not occur under Proposal 5, which merely shifts a growing portion of the MPSERS cost from one government body to another. This shift is irrelevant to the key cost problem, and until this problem is solved, taxpayers face a growing liability.

Ratification of Proposal 5 could distract from a solution if the MPSERS cost problem is seen as having been solved. Proposal 5 would also provide local districts with a payroll subsidy that could intensify the pension problem.

As with the looming MPSERS burden on taxpayers, Proposal 5 does not convincingly address the problem of improving Michigan’s education or restoring Michigan’s economic growth. Decades of relatively high education spending have not led to impressive test results or a nationally competitive state economy.

The proposal could even slow educational and economic recovery. The education spending guaranteed by Proposal 5 would reduce districts’ incentive to attract new students through better educational programs, while the proposal’s additional monies for districts with declining enrollment could encourage some of the state’s academically weakest districts to postpone classroom and fiscal reforms. To the extent that Proposal 5 ultimately added to Michigan’s above-average tax burden, the proposal could also forestall economic prosperity.

The author would like to acknowledge several individuals who reviewed this document and offered numerous helpful suggestions toward its improvement: Michael Williamson, Theodore Bolema, Sean Lewis, Benjamin DeGrow and Ryan Olson.

Additionally, the author would like to thank Kathryn Summers-Coty of the Michigan Senate Fiscal Agency, Mary Ann Cleary of the Michigan House Fiscal Agency, and Tom Clay of the Citizens Research Council of Michigan for their prompt and thorough assistance in answering my questions regarding the research that they have produced on the topics addressed by this report.

The author acknowledges sole responsibility for any mistakes or errors of interpretation.

A LEGISLATIVE INITIATIVE TO ESTABLISH MANDATORY SCHOOL FUNDING LEVELS

The proposed law would:

Increase current funding by approximately $565 million and require State to provide annual funding increases equal to the rate of inflation for public schools, intermediate school districts, community colleges, and higher education (includes state universities and financial aid/grant programs).

Require State to fund any deficiencies from General Fund.

Base funding for school districts with a declining enrollment on three-year student enrollment average.

Reduce and cap retirement fund contribution paid by public schools, community colleges and state universities; shift remaining portion to state.

Reduce funding gap between school districts receiving basic per-pupil foundation allowance and those receiving maximum foundation allowance.

Should this proposed law be approved?

Yes

No

______________________________________________________

INITIATION OF LEGISLATION

An initiation of Legislation to amend 1979 PA 94, entitled "An act to make appropriations to aid in the support of the public schools and the intermediate school districts of the state; to make appropriations for certain other purposes relating to education; to provide for the disbursement of the appropriations; to supplement the school aid fund by the levy and collection of certain taxes; to authorize the issuance of certain bonds and provide for the security of those bonds; to prescribe the powers and duties of certain state departments, the state board of education, and certain other boards and officials; to create certain funds and provide for their expenditure; to prescribe penalties; and to repeal acts and parts of acts." (MCL 388.1601 to 388.1772), by amending the title and section 11 (MCL 388.1611), the title as amended by 2003 PA 158, and section 11 as amended by 2004 PA 351, and by adding sections 12 and 147a.

Existing Michigan law is set forth below. Alterations to

existing provisions of law are set forth below in

BOLD AND UPPERCASE LETTERS

to indicate new language and strike through to indicate deleted language.

THE PEOPLE OF THE STATE OF MICHIGAN ENACT:

Title

An act to make appropriations to aid in the support of the public schools and the intermediate school districts of the state; to make appropriations for certain other purposes relating to education; to provide for the disbursement of the appropriations; TO ESTABLISH MINIMUM FUNDING FOR THE PUBLIC SCHOOLS, THE INTERMEDIATE SCHOOL DISTRICTS, THE COMMUNITY COLLEGES, THE PUBLIC UNIVERSITIES, AND THE INDEPENDENT NONPROFIT COLLEGES OR UNIVERSITIES OF THIS STATE; to supplement the school aid fund by the levy and collection of certain taxes; to authorize the issuance of certain bonds and provide for the security of those bonds; to prescribe the powers and duties of certain state departments, the state board of education, and certain other boards and officials; to create certain funds and provide for their expenditure; to prescribe penalties; and to repeal acts and parts of acts.

Sec. 11. (1) In addition to all other appropriations

under this act for that fiscal year, for the fiscal year ending September 30,

2004, there is appropriated to the state school aid fund from the unreserved

balance in the general fund an amount equal to any deficit balance that would

otherwise exist in the state school aid fund at bookclosing for the fiscal year

ending September 30, 2004. For the fiscal year ending September 30,

20052007,

there is appropriated for the public schools of this state and certain

other state purposes relating to education the sum of $10,909,200,000.00 from

the state school aid fund established by section 11 of article IX of the state

constitution of 1963 and the sum of $264,700,000.00 from the general fund

FROM THE STATE SCHOOL AID FUND THE

SUM NECESSARY TO FULFILL THE REQUIREMENTS OF THIS ACT, AND ANY DEFICIENCY IS

APPROPRIATED FROM THE GENERAL FUND. In

addition, available federal funds are appropriated for each of those

fiscal years THAT FISCAL YEAR.

(2) FOR THE FISCAL YEAR ENDING SEPTEMBER 30, 2007, THE TOTAL AMOUNT APPROPRIATED UNDER THIS ACT FROM STATE FUNDS SHALL NOT BE LESS THAN THE TOTAL AMOUNT APPROPRIATED UNDER THIS ACT FROM STATE FUNDS FOR THE 2004-2005 STATE FISCAL YEAR, ADJUSTED BY THE PERCENTAGE INCREASE IN THE GENERAL PRICE LEVEL FROM THE 2004 CALENDAR YEAR TO THE 2006 CALENDAR YEAR. FOR EACH STATE FISCAL YEAR AFTER THE FISCAL YEAR ENDING SEPTEMBER 30, 2007, THE TOTAL AMOUNT APPROPRIATED UNDER THIS ACT FROM STATE FUNDS SHALL BE INCREASED FROM THE TOTAL AMOUNT FOR THE IMMEDIATELY PRECEDING STATE FISCAL YEAR BY THE PERCENTAGE INCREASE IN THE GENERAL PRICE LEVEL FOR THE CALENDAR YEAR ENDING IN THE IMMEDIATELY PRECEDING STATE FISCAL YEAR. AS USED IN THIS SUBSECTION, "GENERAL PRICE LEVEL" MEANS THE CONSUMER PRICE INDEX FOR THE UNITED STATES AS DEFINED AND OFFICIALLY REPORTED BY THE UNITED STATES DEPARTMENT OF LABOR OR ITS SUCCESSOR AGENCY.

(3)(2)

The appropriations under this section shall be allocated as provided in this

act. Money appropriated under this section from the general fund shall be

expended to fund the purposes of this act before the expenditure of money

appropriated under this section from the state school aid fund. If the