Earlier this year, the legislature debated Governor Engler’s proposal to cut Michigan’s personal income tax rate from the current 4.4 percent to 3.9 percent over five years. Opponents argued that a better way to provide tax relief was to raise the personal exemption. The Governor had the votes, the rate will be cut, and some might say the debate is over.

But the question of which is better—cutting rates or raising exemptions—is still relevant. Explaining why the Governor was right on this one will help illuminate future tax debates and in the meantime, can help us understand the dynamics of taxes and incentives.

Income taxes can be cut by reducing either the tax base (the amount of income subject to the tax) or the tax rate. Increasing the personal exemption is the most common way to reduce the tax base. The personal exemption is subtracted from gross income to determine how much of workers’ income will be subject to the tax. A higher personal exemption means less income is subject to the tax, thus lowering each person’s tax bill. Here’s how that works:

Under Michigan’s current income tax structure, if you have a family of four and you earn $50,000 a year, your first $11,200 of income (the $2,800 personal exemption times four) is exempt from the income tax. The 4.4 percent tax is applied only to the last $38,800 of your annual income.

Now, let’s say you have the opportunity to earn $1,000 of extra income—by working longer hours, by taking a side job, or by saving and investing your money in the stock market or a mutual fund. Every one of those additional dollars of income would be taxed at the 4.4 percent rate. Your reward would be

only $956, not $1,000 (and that’s before all the other deductions for federal income tax, Social Security, etc., which I’ll ignore here for the sake of simplicity).

If the personal exemption was increased to, say, $6,400, more of your income would be exempt ($25,600), so the same 4.4 percent tax would apply only to a smaller share of your current annual income ($24,400). While that would lower the taxes on your current income, it would do nothing to reduce the penalty on earning additional income. Lansing would still take 4.4 percent of it. So, the reward you would receive from putting in the effort to earn that extra $1,000 would still be $956.

If instead the tax rate was reduced to, say, 3.9 percent, although the same amount of your current annual income would be exempt as before ($11,200), each remaining dollar would be taxed at a lower rate.

In addition to lowering your current taxes, cutting the tax rate would also reduce the penalty on earning additional income. Lansing would now take only 3.9 percent of it. The reward you would receive from putting in the effort to earn that extra $1,000 would therefore be higher, $961 instead of $956. While that difference may seem small on an individual basis, over the course of the millions of decisions made throughout Michigan’s economy, the impact would be quite large.

While both methods of reducing personal income taxes will lower current tax bills, they have profoundly different effects on the economy. Regardless of how much the personal exemption is increased, if the tax rate remains unchanged, the tax penalty on additional productive economic activity will remain the same. The only way to reduce that penalty is to cut the tax rate.

With a higher exemption alone, individuals in general would be no more likely to make the effort to work longer hours or to take the risk of saving and investing than they were before. In contrast, lower tax rates encourage more economic activity—greater output, higher incomes, and more jobs.

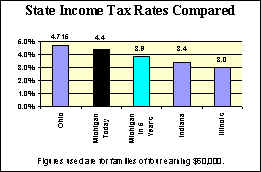

Cutting tax rates will also help make Michigan more competitive with other states. The personal exemption for a family of four in Michigan ($11,200) is already higher than in every other state except Mississippi, while a family of four earning $50,000 faces a higher top tax rate in Michigan than in 18 other states, including nearby Indiana and Illinois.

Bottom line: Michigan did the right thing earlier this year when it moved to cut income tax rates instead of raising the personal exemption. By reducing the penalty on productive economic activity and making Michigan’s tax code more competitive, the result is likely to be greater incentive for economic growth than if the other view had prevailed.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.